All Categories

Featured

Table of Contents

These functions can vary from company-to-company, so make certain to discover your annuity's fatality advantage features. There are several advantages. 1. A MYGA can imply lower tax obligations than a CD. With a CD, the passion you gain is taxed when you earn it, although you do not get it until the CD develops.

So at least, you pay taxes later on, instead than quicker. Not just that, but the intensifying passion will be based upon an amount that has actually not currently been tired. 2. Your recipients will obtain the full account value as of the day you dieand no abandonment costs will be subtracted.

Your beneficiaries can pick either to get the payout in a round figure, or in a series of earnings settlements. 3. Frequently, when somebody passes away, even if he left a will, a judge chooses who obtains what from the estate as occasionally loved ones will say regarding what the will certainly methods.

With a multi-year fixed annuity, the owner has actually clearly assigned a recipient, so no probate is needed. If you add to an Individual retirement account or a 401(k) strategy, you get tax deferral on the incomes, just like a MYGA.

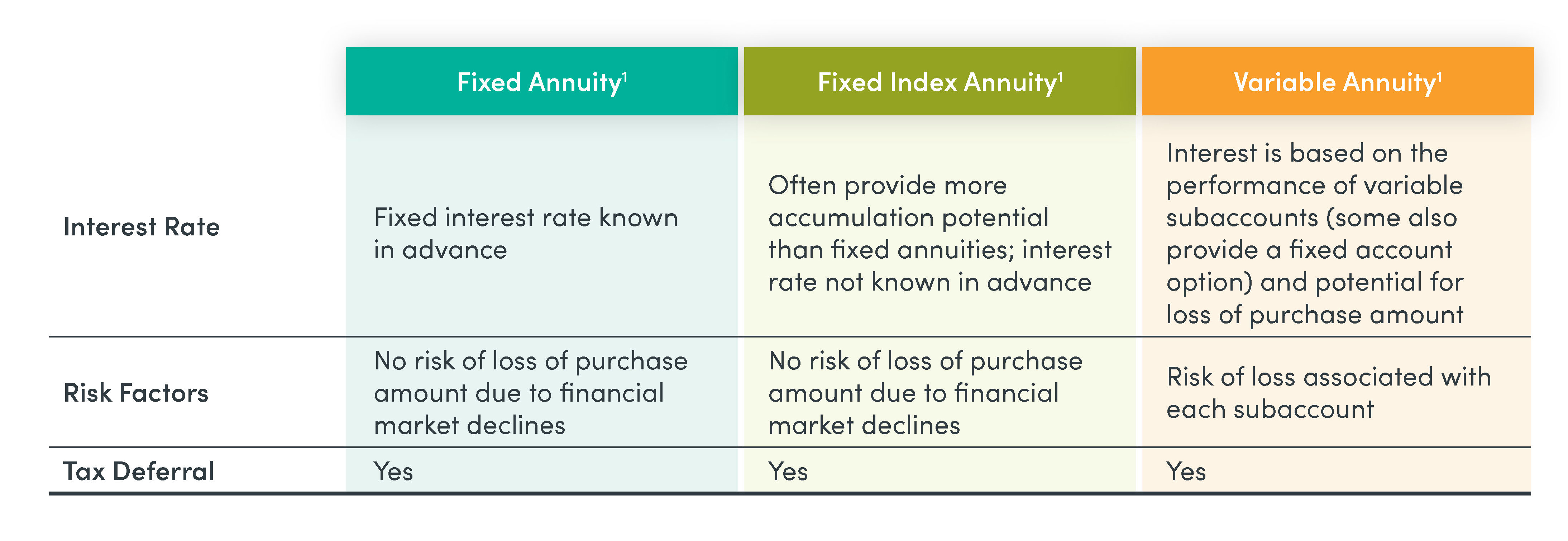

Pension Annuity Comparison

So if you are younger, invest only the funds you will not need up until after age 59 1/2. These could be 401(k) rollovers or money you hold in IRA accounts. Those products already supply tax deferral. MYGAs are fantastic for people who wish to avoid the threats of market variations, and desire a dealt with return and tax deferment.

When you choose on one, the rates of interest will certainly be dealt with and guaranteed for the term you pick. The insurer invests it, usually in high quality lasting bonds, to money your future settlements under the annuity. That's since bonds are rather risk-free. They can additionally invest in stocks. Keep in mind, the insurer is depending not just on your specific repayment to fund your annuity.

These payments are constructed right into the purchase cost, so there are no hidden fees in the MYGA contract. Postponed annuities do not bill costs of any type of kind, or sales costs either. Sure. In the recent setting of low rates of interest, some MYGA investors build "ladders." That indicates purchasing multiple annuities with staggered terms.

Guaranteed Income Life Insurance

For instance, if you opened MYGAs of 3-, 4-, 5- and 6-year terms, you would have an account maturing each year after 3 years. At the end of the term, your cash might be taken out or put into a brand-new annuity-- with good luck, at a greater rate. You can likewise utilize MYGAs in ladders with fixed-indexed annuities, a method that looks for to optimize return while likewise safeguarding principal

As you compare and comparison pictures supplied by numerous insurance provider, take right into consideration each of the locations provided above when making your decision. Comprehending contract terms as well as each annuity's benefits and negative aspects will allow you to make the very best choice for your financial circumstance. Believe carefully about the term.

Annuity Examples Payments

If passion rates have climbed, you may want to secure them in for a longer term. During this time, you can obtain all of your money back.

The company you acquire your multi-year assured annuity with agrees to pay you a fixed rate of interest on your premium amount for your chosen period. You'll get passion attributed regularly, and at the end of the term, you either can renew your annuity at an upgraded rate, leave the money at a repaired account rate, elect a negotiation option, or withdraw your funds.

Annuity Terms And Definitions

Given that a MYGA supplies a set passion price that's ensured for the contract's term, it can provide you with a predictable return. With prices that are set by agreement for a details number of years, MYGAs aren't subject to market fluctuations like other investments.

Minimal liquidity. Annuities commonly have charges for early withdrawal or surrender, which can restrict your capacity to access your cash without costs. Reduced returns than various other financial investments. MYGAs may have lower returns than stocks or mutual funds, which could have greater returns over the long-term. Costs and expenses. Annuities usually have surrender fees and management prices.

MVA is an adjustmenteither favorable or negativeto the gathered value if you make a partial abandonment over the free quantity or fully surrender your contract during the surrender charge duration. Because MYGAs use a fixed rate of return, they may not keep rate with inflation over time.

Fixed Annuity Quotes

MYGA rates can alter typically based on the economic situation, however they're generally higher than what you would gain on a cost savings account. Required a refresher course on the four fundamental kinds of annuities? Find out much more just how annuities can guarantee an income in retired life that you can't outlive.

If your MYGA has market price adjustment provision and you make a withdrawal prior to the term mores than, the firm can readjust the MYGA's surrender value based on modifications in rate of interest - annuity in financial management. If prices have actually boosted since you purchased the annuity, your abandonment worth may decrease to make up the higher rate of interest environment

Annuities with an ROP arrangement usually have reduced guaranteed rate of interest prices to balance out the business's possible threat of having to return the premium. Not all MYGAs have an MVA or an ROP. Conditions rely on the company and the contract. At the end of the MYGA duration you have actually chosen, you have three alternatives: If having actually a guaranteed rates of interest for an established number of years still lines up with your financial strategy, you merely can renew for one more MYGA term, either the same or a different one (if available).

With some MYGAs, if you're uncertain what to do with the cash at the term's end, you don't need to do anything. The built up worth of your MYGA will relocate right into a fixed account with a sustainable one-year rate of interest rate figured out by the business - how variable annuities work. You can leave it there up until you pick your next step

While both deal ensured rates of return, MYGAs commonly use a greater rate of interest than CDs. MYGAs grow tax deferred while CDs are tired as income annually. Annuities expand tax deferred, so you do not owe earnings tax on the earnings till you withdraw them. This permits your profits to worsen over the regard to your MYGA.

With MYGAs, surrender costs might use, depending on the kind of MYGA you pick. You may not only lose interest, but likewise principalthe cash you initially added to the MYGA.

What Is A Fixed Annuity Contract

This suggests you may weary but not the primary quantity added to the CD.Their conservative nature frequently appeals a lot more to people who are coming close to or currently in retired life. They could not be appropriate for everybody. A may be appropriate for you if you desire to: Benefit from an assured rate and lock it in for a period of time.

Take advantage of tax-deferred incomes development. Have the alternative to pick a settlement option for a guaranteed stream of income that can last as long as you live. As with any kind of kind of savings lorry, it is essential to very carefully examine the conditions of the item and speak with to identify if it's a smart choice for attaining your individual requirements and goals.

1All warranties including the death advantage repayments depend on the insurance claims paying capacity of the releasing business and do not use to the investment performance of the hidden funds in the variable annuity. Possessions in the hidden funds undergo market dangers and might change in worth. Variable annuities and their underlying variable investment options are sold by syllabus just.

Level Annuities

This and various other info are included in the program or recap program, if offered, which may be obtained from your investment professional. Please read it prior to you spend or send out cash. 2 Ratings are subject to change and do not apply to the underlying investment choices of variable items. 3 Current tax legislation goes through interpretation and legal modification.

People are urged to look for certain recommendations from their personal tax obligation or legal guidance. By supplying this material, The Guardian Life Insurance Coverage Firm of America, The Guardian Insurance Coverage & Annuity Business, Inc .

{kind=link}

Table of Contents

Latest Posts

Decoding Choosing Between Fixed Annuity And Variable Annuity A Comprehensive Guide to Tax Benefits Of Fixed Vs Variable Annuities Breaking Down the Basics of Investment Plans Features of Fixed Index A

Exploring the Basics of Retirement Options Everything You Need to Know About What Is A Variable Annuity Vs A Fixed Annuity Defining Fixed Indexed Annuity Vs Market-variable Annuity Pros and Cons of Re

Highlighting Fixed Income Annuity Vs Variable Annuity A Closer Look at How Retirement Planning Works Breaking Down the Basics of Investment Plans Features of Smart Investment Choices Why Choosing the

More

Latest Posts